Ukrainian companies and companies with significant Ukrainian exposure in which you can invest

Ukrainian companies and companies with significant Ukrainian exposure in which you can invest

Ukrainian exposure can be obtained not only with direct investments in Ukrainian assets but also through different Ukrainie-exposed stocks and Eurobonds / military bonds.

Astarta Holding N.V (ASTH, WSE)

One of the largest agro-industrial holdings in Ukraine:

At the beginning of the full-scale invasion, Astarta's shares lost nearly 70% of their value compared to their early 2022 levels. While the stock price stood at 26 PLN in May 2024, it demonstrated a rapid recovery thereafter, peaking at 64 PLN by May 2025. By the end of 2025, the price stabilized, with December values fluctuating between 44 and 45 PLN which is 10% higher than the pre-war estimate.

The annual financial report for Astarta gave hints on how the company was doing in 2024. Revenue reached EUR 612 mln, compared to EUR 619 mln in 2023. EBITDA grew to EUR 159 mln from EUR 145 mln in the previous year, representing a (+10%) increase. The Sugar segment became the primary driver, with production reaching a seven-year high of 380 kt (+1% y-o-y) and exports increasing four-fold. While grain and oilseeds production decreased to 561 kt, Cattle Farming showed resilience with milk production rising to 119 kt. This improved profitability, despite stable revenue, was driven by optimized logistics via sea corridors and efficient cost management.

Ovostar Union N.V. (OVO, WSE)

One of the largest egg producers in Europe:

From the beginning of 2022 to its lowest point, OVOSTAR's share price lost up to 45% of its original value. However, from the start of 2023 to May 2024, the price increased by over 50%, reaching 67.80 PLN. Since then, the stock has maintained its recovery, and as of early 2026, the price continues to fluctuate within the 68–70 PLN range, holding steady above its pre-invasion levels.

MHP (MHPCq, LSE)

MHP is the largest integrated Ukrainian producer and exporter of poultry and crops, as well as other meat and sausage products and ready-to-eat meat products.

The company specializes in the production of poultry and, in particular, the cultivation of cereals:

In 2024, the group's revenue reached a record $3,046 million, with export revenue accounting for $1,840 million or 60% of the total. Adjusted EBITDA significantly improved to $566 million, resulting in a margin increase to 19%.

Mlk Foods Public Company Ltd / Milkiland (MLK, WSE )

MLK Foods is an international dairy producer with core operations in the CIS and EU:

Stock prices have fallen 67% from the end of 2021 to the lowest point in 2022 year and additionally lost 35% from the beginning of the 2023 till May 2024. Starting in June 2024, prices began to rise and reached pre-war levels.

IMC SA (IMC, WSE)

IMC – is among top 10 Ukrainian agriculture companies operating 120 thousand hectares of arable land in key farming regions of Ukraine (Poltava, Chernihiv, Sumy).

In 2024, revenue increased from USD 139.5 to 211.3 mln (+51%) y-o-y. EBITDA significantly recovered, increasing from USD 3.2 to 86.1 mln, driven by the stabilization of market prices and improved operational efficiency. Net profit also returned to positive territory, reaching USD 54.5 mln in 2024 compared to a net loss of USD 21.0 mln in the previous year.

EPAM Systems Inc (EPAM, NYSE)

EPAM is IT company named a Forbes global 2000 company in 2011, works in over than 50 countries:

IIn 2024, EPAM's revenue reached USD 4,728 million, representing a slight recovery of 0.8% from USD 4,691 million in 2023 (a year that saw a minor decline due to the company's exit from Russia). Net income also showed resilience, rising to USD 454.6 million in 2024, an increase of 9% compared to USD 417.1 million in the previous year.

KSG-Agro (KSG, WSE)

KSG-Agro is one of Ukraine's leading agribusiness holdings, engaged in grain cultivation, oilseed production, and livestock farming:

Military Bonds

Ukraine has issued a series of war bonds to raise financing and support the army. These bonds can be purchased by Ukrainian legal entities and individuals, as well as foreign investors who want to support Ukraine. The bonds can be nominated and purchased in UAH, USD, or EUR. The first auction of 2026, held on January 6, was highly successful, raising UAH 16.2 billion (equivalent).

Currently, Ukrainian war bonds offer yields of up to 17.8%, significantly outperforming US Treasury bills, which now offer a maximum yield of approximately 3.65%.

Canada Ukraine Sovereignty Bond

If you want to support Ukraine with your investment, the Ukraine Sovereignty Bond remains a stable and secure option. These are five-year bonds issued by the Government of Canada for CAD 500 million, with a maturity date set for August 24, 2027.The bonds are issued in Canadian dollars and carry a fixed interest rate of 3.245%, with coupon payments made semi-annually. While the initial offering is complete, these bonds continue to trade, and the Canadian government has already transferred the collected funds to Ukraine through the IMF Administered Account to support essential state services. As these are backed by Canada’s AAA credit rating, they offer a low-risk way to contribute to Ukraine's financial resilience as the bonds approach their final 18 months of circulation.

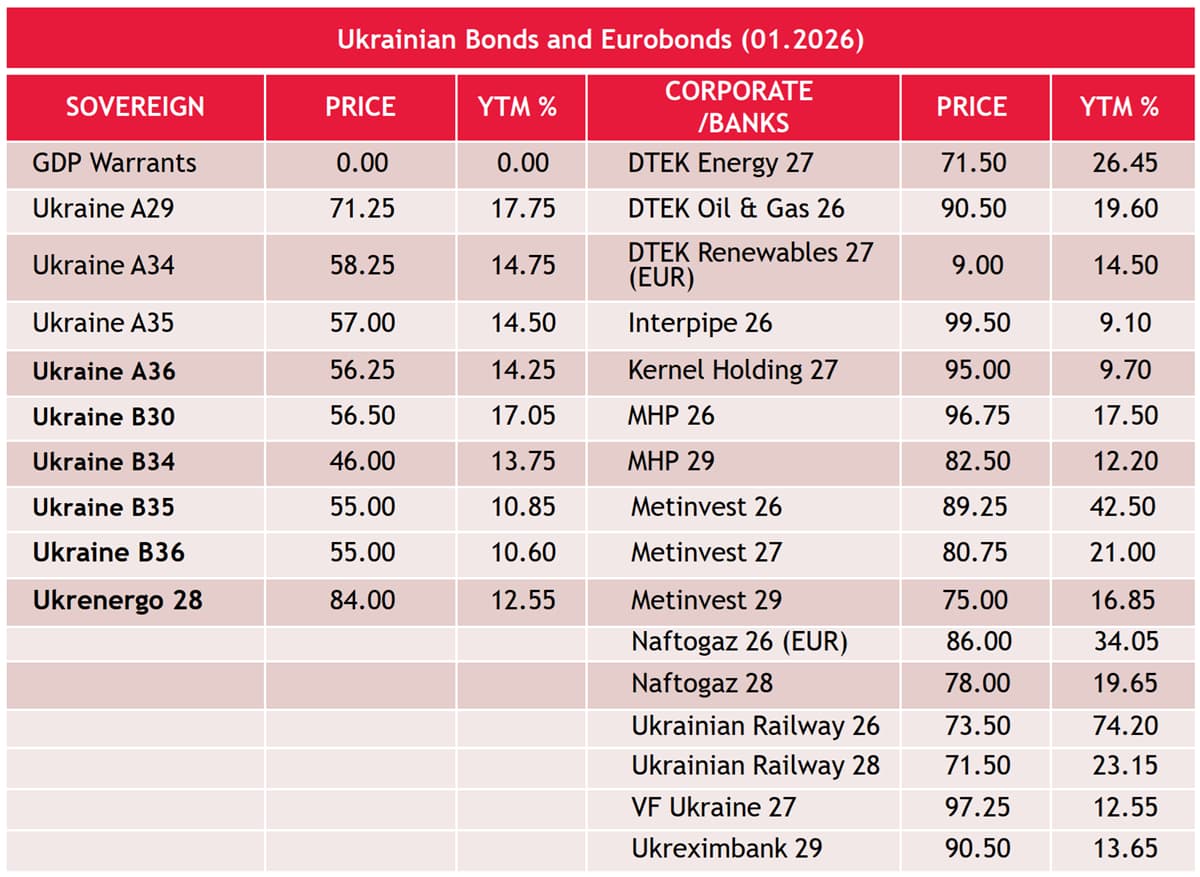

Ukrainian Eurobond

Ukrainian sovereign Eurobonds have been under significant pressure since the onset of the war. Approximately 50% of the Ukrainian budget (specifically its social component, excluding the military) is supported by international donors. Given this, restructuring of at least the upcoming issues seems plausible.

There's also a unique instrument – the GDP-linked Warrants. In 2015, Ukraine issued GDP warrants worth $3.6 billion to make its restructuring of $15 billion of debt more appealing. This restructuring required investors to write off 20% of the original value of their assets. However, these warrants provide a potential benefit linked to GDP growth between 2021 and 2040. If the real, inflation-adjusted GDP growth surpasses 3%, Ukraine commits to paying warrant holders an amount equivalent to 15% of the economic output exceeding this threshold. This percentage escalates to 40% if the growth surpasses 4%.

Eurobonds from the corporate and banking sectors have demonstrated better resilience compared to the sovereign ones, attributed mainly to a healthier financial situation. This is particularly true for the banking sector, where liquidity has reached an all-time high, thanks to successful reforms implemented between 2015 and 2016. Some entities, like MHP, plan to repurchase a portion of their own bonds, viewing it as a strategic investment given the prevailing circumstances.

.jpg)